Executive Summary: The Anatomy of a Market Failure

The global semiconductor memory market is currently navigating a period of unprecedented structural dislocation. As of late 2025, the convergence of aggressive artificial intelligence (AI) infrastructure expansion and a contraction in legacy manufacturing capacity has precipitated a severe pricing surge in Dynamic Random Access Memory (DRAM). This report provides an exhaustive analysis of the “RAM price hike” of 2025, a phenomenon characterized by triple-digit percentage increases in consumer memory costs, the strategic exit of major suppliers from the retail market, and a fundamental reshaping of the supply chain that prioritizes enterprise AI over consumer electronics.

The current market environment, often referred to by industry analysts as a “memory supercycle,” is distinct from previous cyclical upturns. Unlike the supply shocks of 2017-2018 or the demand spikes associated with cryptocurrency mining, the 2025 crisis is driven by a permanent reallocation of silicon wafer capacity toward High Bandwidth Memory (HBM). This shift has created a zero-sum game where the production of AI accelerators directly cannibalizes the supply of standard DDR5 and DDR4 modules.

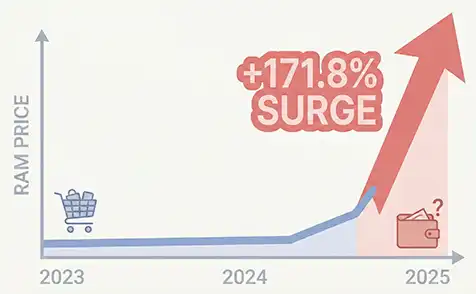

Retail data from the fourth quarter of 2025 indicates that the average selling price (ASP) of consumer RAM kits has increased by approximately 171.8% year-over-year. In specific high-demand segments, such as low-latency DDR5-6000 memory favoured by gamers, prices have nearly tripled. The volatility is such that major retailers have abandoned fixed pricing models in favor of dynamic, market-based pricing, fluctuating daily based on distributor availability.

This report draws upon extensive market data, supply chain leaks, and financial reports to analyze the root causes of this inflation, the mechanics of the current shortage, and the strategic outlook for 2026 and 2027. It offers actionable advice for consumers, system integrators, and investors navigating a hyper-inflationary hardware market.

1. The Macro-Economic Landscape: A Perfect Storm

The “RAM price hike” is not an isolated event but the result of a confluence of macroeconomic factors and industry-specific pivots. To understand the severity of the 2025 crisis, one must analyze the broader semiconductor landscape.

1.1 The End of the Glut and the Rise of the Supercycle

Following the post-pandemic demand collapse of 2023 and early 2024, memory manufacturers—principally Samsung, SK Hynix, and Micron—instituted severe production cuts to stabilize plummeting prices. These cuts, intended to reduce inventory overhang, successfully normalized the market by early 2025. However, the industry failed to anticipate the velocity of the AI infrastructure build-out.

As hyperscalers like Microsoft, Google, and Meta accelerated their procurement of AI servers, the demand for memory did not merely recover; it exploded. This initiated a “supercycle,” a prolonged period of demand exceeding supply, driving prices upward for an extended duration. Analysts predict this cycle could last significantly longer than typical 18-month booms, potentially extending through 2027 or 2028.

The structural difference in this supercycle is the “wafer penalty” of AI memory. producing HBM3e and HBM4 requires significantly more cleanroom space and wafer starts than standard DRAM. Industry reports suggest that producing a given capacity of HBM requires roughly three times the wafer output of conventional DRAM due to larger die sizes and lower yields associated with complex Through-Silicon Via (TSV) stacking. This physical reality means that even as fabs run at full utilization, the total bit output available for the consumer market is shrinking.

1.2 The “Stargate” Effect: Hyperscaler Dominance

A critical driver of the shortage is the sheer scale of procurement by AI entities. OpenAI’s “Stargate” project and similar massive data center initiatives have effectively cornered the global supply of high-performance DRAM. Reports from late 2025 indicate that OpenAI alone secured exclusive supply deals with Samsung and SK Hynix that account for nearly 40% of the planet’s available DRAM capacity.

This level of consolidation is unprecedented. In previous cycles, no single entity commanded enough purchasing power to disrupt global supply chains single-handedly. Today, the “AI overlords” are booking allocations well into 2026 and 2027, filling Tier-1 order books to an effective 70% capacity. This leaves the “spot market”—where consumer brands like Corsair, G.Skill, and Kingston procure their chips—fighting for the remaining 30% of supply against smartphone manufacturers, automotive OEMs, and industrial users.

1.3 Inventory Collapse and Just-in-Time Failure

The buffer stock that traditionally smooths out price volatility has evaporated. Throughout 2024, suppliers maintained healthy inventory levels of 13-17 weeks. By October 2025, these inventories had collapsed to a critical low of 2-4 weeks.

This collapse represents a failure of “Just-in-Time” (JIT) manufacturing principles in the face of a secular demand shock. With no warehouse buffer, every minor disruption—whether a logistics delay or a yield issue at a fab—translates immediately into retail price spikes. This precarious position has triggered panic buying among downstream OEMs. Major PC manufacturers like Lenovo and Dell, foreseeing the shortage, reportedly “bought the supply chain dry” months in advance, holding inventory levels 50% higher than usual. This hoarding behavior exacerbates the scarcity for smaller players and DIY consumers, creating a feedback loop of rising prices and panic.

2. Supply-Side Analysis: The Cannibalization of Consumer DRAM

The 2025 RAM price hike is fundamentally a supply-side crisis. It is not that consumers are buying significantly more PCs; rather, the industry has stopped making enough RAM for them.

2.1 The HBM Pivot: Profitability Over Volume

The three major memory manufacturers operate as an oligopoly, and their strategic priorities have shifted entirely to the high-margin AI sector. HBM yields significantly higher profit margins than commodity DDR5. Samsung, for example, reportedly earns a ~60% margin on HBM products compared to fluctuating margins on standard DRAM.

Consequently, fabs are being retooled. Samsung is actively converting production lines that previously manufactured DDR4 and DDR5 to produce HBM logic dies and memory stacks. This reallocation is estimated to have removed approximately 30-40% of the company’s commodity DRAM capacity. For a market that relies on Samsung for a plurality of its supply, this is a catastrophic reduction in availability.

Table 1: Estimated Global DRAM Production Reallocation (2024 vs. 2025)

| Production Segment | 2024 Capacity Allocation | 2025 Capacity Allocation | Change | Impact on Pricing |

| Commodity DDR4 | 35% | 15% | -57% | Extreme Inflation |

| Commodity DDR5 | 40% | 30% | -25% | High Inflation |

| LPDDR5/5X (Mobile) | 20% | 25% | +25% | Moderate Inflation |

| HBM (AI/HPC) | 5% | 30% | +500% | Premium Pricing |

Source: Derived from TrendForce and industry reports.

The table illustrates a massive shift away from DDR4 and standard DDR5. The 500% increase in HBM allocation comes directly at the expense of the legacy and mainstream PC markets. The reduction in DDR4 capacity is particularly punishing, as it creates a “scarcity tax” on budget builders who rely on older platforms.

2.2 The Micron/Crucial Exit: A Structural Blow

In December 2025, the market received a clear signal of the industry’s new direction: Micron Technology announced the discontinuation of its consumer-facing “Crucial” brand for DRAM and SSDs. For decades, Crucial served as a stabilizing force in the market, offering reliable, direct-to-consumer memory at MSRP.

Micron’s exit is not a sign of failure but of ruthlessly efficient capital allocation. The company has calculated that the resources used to package, market, and distribute consumer modules are better spent servicing hyperscaler contracts. This exit removes a massive volume of supply from the retail channel and, crucially, removes a price anchor. Without Crucial’s baseline pricing, competitors face less pressure to keep prices low, allowing for more aggressive markups from remaining third-party brands.

2.3 The Deterioration of Yields and Binning

The rush to ramp up production of high-speed DDR5 and HBM has also put pressure on silicon yields. As manufacturers push for higher speeds (DDR5-8000+), the “binning” process becomes more selective. Only the highest-quality silicon can meet the strict timing and voltage requirements of enthusiast kits.

However, the “golden samples” that would typically be sold as premium consumer kits (like G.Skill Trident Z5 Royal) are increasingly being diverted to enterprise applications where stability at high temperatures is paramount. This leaves the consumer market with a bimodal distribution: expensive, scarce high-performance kits, or widely available but mediocre “standard” bin kits. The middle ground—affordable high-performance RAM—has effectively vanished.

3. Price Analysis: The “Seafood Market” Reality

The volatility of RAM prices in late 2025 has forced a paradigm shift in how retailers price components. The stability of the past decade has been replaced by hyper-dynamic pricing models.

3.1 Daily Price Fluctuations

Reports from major electronics hubs, such as Akihabara in Japan and Silicon Valley in the US, describe a retail environment akin to a commodities exchange. Retailers like Central Computers have implemented “market pricing” for RAM, explicitly comparing it to buying lobster at a seafood market. Prices are updated daily based on the replacement cost from distributors.

This volatility makes budgeting for a PC build nearly impossible. A quote generated on a Monday may be invalid by Wednesday. This uncertainty fuels “Fear Of Missing Out” (FOMO), causing consumers to purchase components prematurely or hoard them, further straining supply.

3.2 The DDR4 “Echo Bubble”

A counter-intuitive aspect of the 2025 crisis is the surge in DDR4 prices. Typically, as a memory standard becomes obsolete, its price drops until it hits a production floor. However, because manufacturers have aggressively cut DDR4 capacity to free up space for HBM, the supply of DDR4 has fallen faster than the demand.

By late 2025, a standard 32GB DDR4-3600 kit, previously the gold standard for budget builds, saw its price more than double from ~$70 to ~$161. This “echo bubble” is particularly damaging because it hits the most price-sensitive segment of the market: students, budget gamers, and users upgrading older AM4 or LGA1200 systems. The price parity between DDR4 and DDR5 has now been reached in many regions, destroying the value proposition of staying on older platforms.

3.3 Regional Price Disparities

The impact of the RAM price hike is not uniform globally. While the US has seen increases of roughly 163% for certain kits, other markets have faced even steeper inflation due to currency fluctuations and logistics prioritization.

Table 2: Global Regional Price Impact for 32GB DDR5 Modules (Q4 2025)

| Region | Retailer Example | Price Increase (Sept-Dec 2025) | Local Market Factors |

| United States | Newegg | +163% | High demand, strong dollar buffers some import costs. |

| United Kingdom | Overclockers UK | +219% | Post-Brexit logistics friction, weaker pound. |

| Germany | Mindfactory | +173% | Eurozone inflation, VAT impact. |

| Japan | Kakaku | +619% | Extreme currency devaluation (Yen), import reliance. |

| France | LDLC | +275% | High taxes, strict consumer protection laws limiting dynamic pricing speed. |

Source: Market analysis derived from regional pricing reports.

The data highlights that Japanese consumers are facing a catastrophic 619% increase, likely exacerbated by the weakness of the Yen against the Dollar, the currency in which global DRAM contracts are settled. This suggests that for international buyers, the “RAM price hike” is compounded by macroeconomic currency wars.

4. The Demand-Side Shock: AI PCs and the NPU

While supply constraints are the primary driver of the RAM price hike, the nature of demand is also shifting. The 2025 PC market is defined by the “AI PC,” a device class that requires significantly more memory than its predecessors.

4.1 The Unified Memory Hunger

Modern processors, such as Intel’s Lunar Lake (Core Ultra Series 2) and AMD’s Strix Point (Ryzen AI 300 series), utilize a unified memory architecture. In this design, the CPU, Integrated GPU (iGPU), and Neural Processing Unit (NPU) all share the same pool of system RAM.

Unlike a discrete GPU which has its own VRAM, the NPU in an AI PC must carve out its workspace from the system RAM. For basic AI tasks (Microsoft Copilot+, approx. 40 TOPS), a significant portion of memory is reserved for model weights and inference buffers.

- The 16GB Trap: While 16GB is marketed as the baseline for AI PCs, it is functionally obsolete for enthusiasts. The Windows OS, browser overhead, and background applications consume 8-10GB. If a local Large Language Model (LLM) like Llama 3 8B requires 6-8GB of VRAM/RAM to load, a 16GB system will immediately thrash to the swap file, destroying performance.

- The 32GB Minimum: Consequently, 32GB has become the new functional baseline for any user intending to utilize local AI features. This doubles the bit demand per PC unit at the exact moment supply is contracting.

4.2 High-Speed Requirements

It is not just capacity; it is speed. AI inference is highly bandwidth-sensitive. To feed an NPU capable of 50 TOPS, the memory must be fast. AMD’s Strix Point APUs have been updated to support LPDDR5X-8000 speeds to provide the necessary bandwidth for their XDNA 2 NPUs.

This reliance on high-speed LPDDR5X creates a conflict. LPDDR memory is typically soldered, meaning it cannot be upgraded by the user. Consumers are forced to configure their laptops with 32GB or 64GB at the point of purchase. Manufacturers, aware of this, are charging exorbitant premiums for these high-RAM SKUs, effectively utilizing the “RAM price hike” to increase their average selling prices (ASPs).

4.3 Software Bloat and the “Electron” Era

Beyond AI, general software bloat continues to drive memory demand. The prevalence of Electron-based apps (Discord, Slack, VS Code) means that even “light” workloads are memory-intensive. For gaming, titles utilizing Unreal Engine 5 are increasingly listing 32GB as a “Recommended” spec, further pushing gamers toward expensive upgrades. The days of 16GB being “enough for gaming” are definitively over in the 2025 landscape.

5. The Consumer Impact: Psychology and Survival

The combination of rising prices and tech-driven necessity has created a volatile psychological environment for consumers.

5.1 FOMO and Panic Buying

The rapid escalation of prices has triggered a wave of panic buying. Consumers who were planning upgrades for 2026 are pulling their purchases forward, fearing that prices will double again. This behavior acts as a self-fulfilling prophecy, draining retail channels of inventory and validating retailers’ decisions to raise prices further.

Social media platforms like Reddit are filled with users validating each other’s panic. Posts discussing “RAM stashes” and showing off stockpiles of DDR5 kits contribute to a sense of scarcity. This “hoarding” mentality is not limited to individuals; small system integrators and local computer shops are also stockpiling kits to protect their margins on future builds.

5.2 The Scalper Economy

Inevitably, the shortage has attracted scalpers. Unlike the GPU crisis where bots targeted specific product launches, the RAM scalping market is broader. Automated scripts sweep online retailers for any DDR5 kit priced below the current “street value.”

These kits then reappear on secondary markets like eBay at significant markups. Data from late 2025 shows used DDR5 kits selling for 50-100% more than their original MSRP. Scalpers are exploiting the “sold out” status at major retailers to force desperate builders into the secondary market. A 32GB kit that retailed for $90 in early 2025 is effectively a liquid asset, traded with the same ferocity as a speculative stock.

5.3 The Pre-Built Arbitrage

One anomaly in the market is the pricing of pre-built PCs. Large OEMs like Dell, HP, and Lenovo negotiate long-term supply contracts with fixed pricing. As a result, the price of their pre-built systems often lags behind the spot market by 3-6 months.

In late 2025, it became cheaper in some instances to buy a pre-built PC with 32GB of RAM than to build a custom PC with the same specifications. This “inventory lag” provides a temporary loophole for consumers, although SIs like CyberPowerPC have already begun to adjust their pricing to reflect the new reality.

6. Future Outlook: 2026-2027

When will the “RAM price hike” end? The outlook is sobering. The structural nature of the shortage suggests that relief is not imminent.

6.1 The “Longer and Stronger” Cycle

Most analysts, including those from TrendForce and TeamGroup, predict that the shortage will persist through the first half of 2026. Some more bearish forecasts suggest the “supercycle” could extend into 2027 or 2028.

- H1 2026: Prices are expected to remain at their peak or continue rising slightly as hyperscalers consume the majority of the year’s production.

- H2 2026: Potential stabilization may occur if AI demand moderates or if new fab capacity comes online. However, building a fab takes years, not months.

- 2027: This is the earliest realistic window for a return to “normal” pricing, contingent on the successful ramp-up of new production nodes.

6.2 The Transition to DDR6

Looking further ahead, the industry is preparing for DDR6. JEDEC specifications suggest DDR6 will debut around 2027 with speeds ranging from 8,800 MT/s to 17,600 MT/s. While this promises a massive performance leap, it also requires significant R&D investment.

The development of DDR6 may actually exacerbate the current shortage. Engineering resources and pilot lines that could be used to squeeze more yield out of DDR5 are instead being diverted to valid DDR6 and HBM4 architectures. This suggests that the industry is focused on the next generation of high-margin products rather than solving the supply constraints of the current generation.

6.3 CAMM2 Adoption

The adoption of CAMM2 (Compression Attached Memory Module) was expected to accelerate in 2025/2026. However, high DRAM costs have slowed this transition. Motherboard manufacturers are hesitant to introduce a new, expensive socket standard when the memory itself is already prohibitively expensive. We expect CAMM2 to remain a niche high-end solution for premium laptops until DDR6 becomes the standard, likely pushing widespread adoption to 2027.

7. Strategic Advice: The Survival Guide

Given the hostile market conditions, consumers and businesses must adopt new strategies. The old rules of “wait for a sale” no longer apply.

7.1 Buying Advice (Buy vs. Wait)

Verdict: BUY NOW (with caveats).

- For New Builds: If you require a PC in the next 6-9 months, purchase your RAM immediately. The consensus is that prices will rise further in Q1/Q2 2026. Waiting for a “Black Friday” deal is a gamble with poor odds, as retailers have no incentive to discount scarce stock.

- For Upgrades: If you are on 16GB of DDR5, upgrade to 32GB or 64GB now. The “opportunity cost” of waiting is high.

- The “Good Enough” Strategy: Do not chase the highest speeds. The price premium for DDR5-7200 or 8000 is disproportionate to the performance gain. Settle for a reliable DDR5-5600 or 6000 kit. The money saved is better spent on a GPU or SSD.

- Pre-Built Option: Seriously consider a pre-built system from a major OEM if the component prices in your region are scalper-level. You may find that the sum of the parts is greater than the whole price of a Dell or Lenovo tower.

7.2 Selling Advice (Hold vs. Sell)

Verdict: SELL SPARE KITS / HOLD MAIN RIG.

- The “Asset” Play: If you have spare DDR5 kits sitting in a drawer, now is the time to sell. Prices are at a local maximum, and demand is feverish. You can likely sell used kits for near-retail prices on eBay or enthusiast forums.

- Do Not Liquidate Essentials: Do not sell the RAM from your primary rig hoping to buy it back cheaper later. The market is too volatile, and you risk being priced out of your own hardware.

- DDR4 Liquidation: If you have high-quality B-die DDR4 kits, they are currently fetching a premium from users trying to squeeze life out of AM4 systems. This is a good time to exit the DDR4 market if you are planning a platform upgrade in 2027.

7.3 Investment Perspective

For those looking at the market from an investment angle, the “RAM price hike” signals a broader inflationary trend in computing.

- Stockpiling: For small businesses or LAN centers, stockpiling replacement RAM now is a sound hedge against 2026 inflation.

- Component Prioritization: In budgeting for 2026 projects, allocate a higher percentage of CaPex to memory. Expect RAM to consume 20-25% of the total system cost, up from the traditional 10-15%.

8. Conclusion

The 2025 RAM price hike is a stark reminder of the fragility of the global electronics supply chain. It is a crisis manufactured by the industry’s pivot to AI, exacerbating the scarcity of consumer goods to fuel the data center boom. The era of cheap, abundant memory is over, at least for the medium term.

For the consumer, the “RAM price hike” forces a re-evaluation of value. The budget build is dead; the 16GB laptop is a trap; and the scalper is the new retailer. Navigating this landscape requires decisiveness: buy what you need now, hold what you have, and adjust your expectations for the cost of computing in the age of AI. The supercycle is here, and it will exact its toll in silicon and gold.

9. Appendix: Technical Data & Reference Tables

9.1 Comparative Price Evolution of DDR5 Memory Kits (September – November 2025)

| Memory Specification | Target Demographic | Price (Sept 2025) | Price (Nov 2025) | % Increase |

| DDR5-6000 CL30 (2x16GB) | Mainstream Gaming | ~€140 ($149) | ~€265 ($285) | +89% |

| DDR5-6400 CL32 (2x16GB) | High-End Enthusiast | ~€150 ($160) | ~€250 ($265) | +66% |

| DDR5-6400 CL30 (2x16GB) | Prosumer Workstation | ~€190 ($200) | ~€390 ($415) | +105% |

| G.Skill Specific High-Bin | Overclocking | ~€145 ($155) | ~€345 ($365) | +138% |

9.2 Global Regional Price Impact for 32GB DDR5 Modules (Q4 2025)

| Region | Retailer Example | Price Increase (Sept-Dec 2025) | Local Market Factors |

| United States | Newegg | +163% | High demand, strong dollar buffers some import costs. |

| United Kingdom | Overclockers UK | +219% | Post-Brexit logistics friction, weaker pound. |

| Germany | Mindfactory | +173% | Eurozone inflation, VAT impact. |

| Japan | Kakaku | +619% | Extreme currency devaluation (Yen), import reliance. |

| France | LDLC | +275% | High taxes, strict consumer protection laws limiting dynamic pricing speed. |

Source: Market analysis derived from regional pricing reports.

9.3 Estimated Global DRAM Production Reallocation (2024 vs. 2025)

| Production Segment | 2024 Capacity Allocation | 2025 Capacity Allocation | Change | Impact on Pricing |

| Commodity DDR4 | 35% | 15% | -57% | Extreme Inflation |

| Commodity DDR5 | 40% | 30% | -25% | High Inflation |

| LPDDR5/5X (Mobile) | 20% | 25% | +25% | Moderate Inflation |

| HBM (AI/HPC) | 5% | 30% | +500% | Premium Pricing |

Related articles –

Is Upgrading a 10-Year-Old Laptop Worth It? The 5-Point Test You Must Take

Run Your Own ChatGPT: The Ultimate Guide to Local LLMs in 2026